Navigating Shifts in Consumer Behaviour

This article was originally intended for the Corvus Magazine

Hey everyone! It's been a minute since I last wrote anything, and I'm sorry about that. Life's been busy with studying for an exam and starting a new job.

But I have something exciting to share with you today. I wrote an article for Corvus Magazine, but due to some delays, I thought it would be great to share it with you all instead. So, take a look - it's definitely a fascinating read!

Blockbuster was once the undisputed leader of the video rental industry during the late 1990s. With over 9,000 stores spread across the world, a massive workforce of 84,000 employees, and a staggering 65 million registered customers, the company was valued at an impressive $3 billion at its peak. In just one year, Blockbuster earned a whopping $800 million from late fees alone. Its cultural influence was undeniable, with hordes of people flocking to Blockbuster stores on weekends to rent the latest films and enjoy a cosy night in with their loved ones.

However, the emergence of Netflix in 1997 marked the beginning of a major disruption that would eventually bring down the giant. With its online subscription service, Netflix capitalized on consumers' desire for convenience and instant access, quickly adapting to the shift and leaving Blockbuster behind with its outdated brick-and-mortar model and late fees. As a result of its inability to keep up, Blockbuster went bankrupt in 2010.

Being adaptable and responsive to changes in consumer behaviour is a crucial aspect of running a successful business. This is exemplified by the downfall of Blockbuster. However, companies such as Starbucks, Amazon, Unilever, and Procter and Gamble (P&G) have demonstrated their ability to effectively adapt to these shifts in consumer behaviour, leading them to become industry leaders.

P&G, the world's second-largest consumer goods company, has a remarkable legacy of over 180 years in the industry. Despite facing various challenges over the decades, such as increased competition from established rivals and new market entrants, and criticism over its environmental impact and use of potentially harmful chemicals in some of its products, P&G has consistently demonstrated resilience and innovation. The company has invested heavily in research and development to create new and innovative products that meet consumers' evolving needs and preferences. This investment has paid off in emerging markets such as China, where Pampers, a key consumer product for the company, transformed from having little market acceptance to becoming the number one-selling diaper brand in the country, generating almost $1 billion in revenue for the company as of 2021.

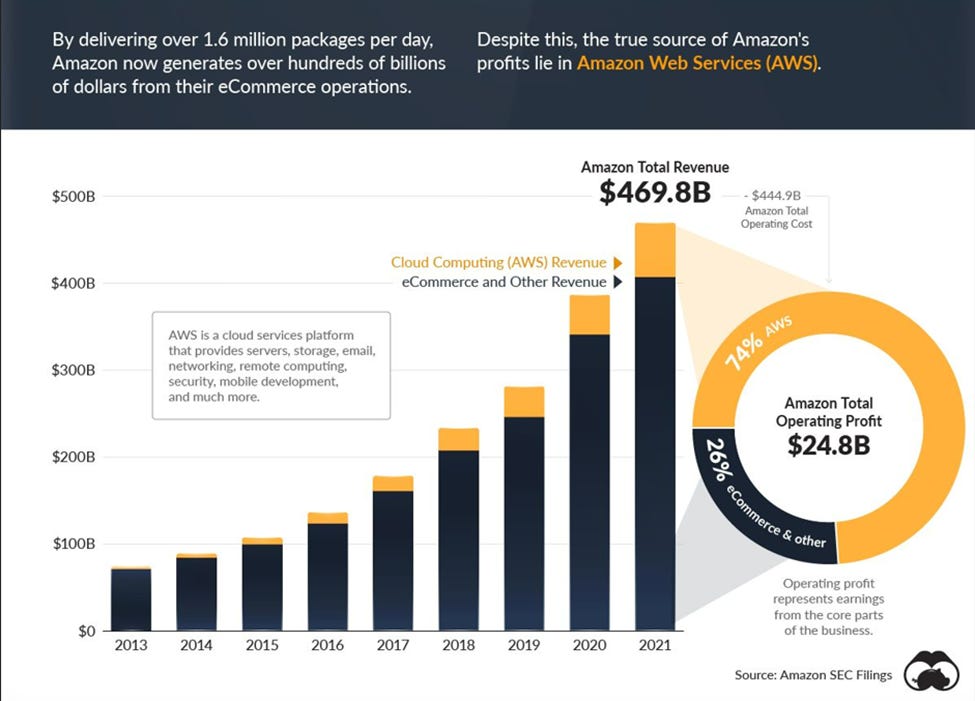

Amazon, founded in 1994, started as an online bookstore and quickly expanded its offerings to include a wide range of products as consumer interest in e-commerce grew. Amazon has demonstrated its ability to remain adaptable and innovative, enabling it to navigate shifts in consumer behaviour and stay ahead of the competition. The company continues to invest in emerging technologies and services, such as Amazon Web Services (AWS), its cloud computing division, which was started in 2006, to diversify its revenue stream. The division now contributes up to 13.2% of the company’s revenue.

Amazon has been able to maintain its position as a leading e-commerce and technology company for over two decades by consistently staying innovative and responsive to customer demands. The resounding success of companies like P&G and Amazon serves as a powerful reminder that adapting to changing consumer behaviour is not just important, but essential for achieving long-term success.

Post-Covid Trend in Consumer Behaviour

The COVID-19 pandemic has had a profound impact on consumer behaviour and decision-making, leading to significant changes in the global economy. As a result, digital services and online shopping have become increasingly popular, and this trend is only expected to grow. In fact, by 2023, online shopping is projected to contribute to 22% of global retail sales. Despite this surge in online shopping, consumers still prefer a blended experience, with 45% opting for in-store shopping.

Moreover, consumers are now conducting more thorough research before making a purchase, focusing on price comparisons, online reviews, and social media mentions. According to a study by GE Capital, 81% of retail shoppers conduct online research before buying. Personalization has also become a crucial factor in consumer behaviour, with customers expecting brands to provide customized experiences that cater to their unique needs and preferences. A recent survey by McKinsey found that 71% of consumers anticipate personalization from companies, and 76% become annoyed when this does not occur. Therefore, it is of utmost importance for brands to focus on the consumer to be perceived as authentic and responsive to their needs.

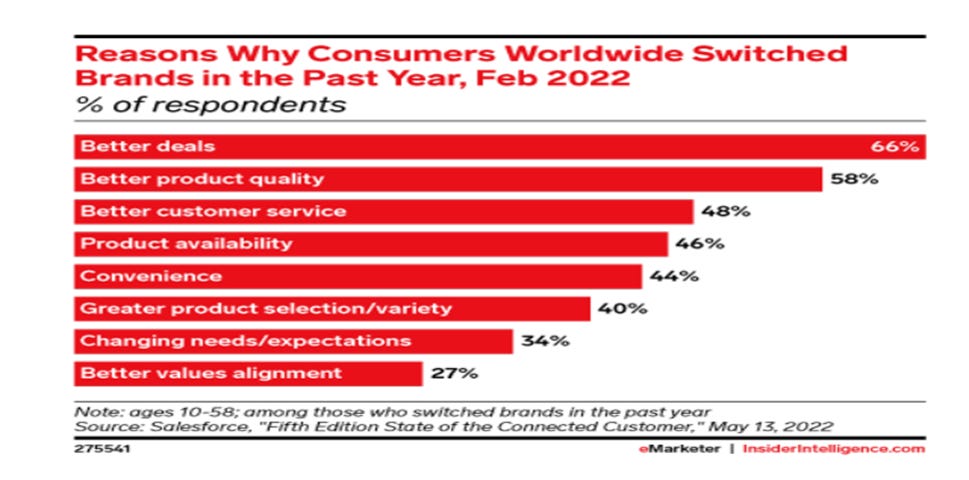

As inflation concerns continue to take centre stage, there has been a clear and unmistakable increase in consumers switching brands. The latest data reveals that an astounding 71% of consumers worldwide have switched brands at least once in 2021. This trend underscores the vital importance of companies maintaining a competitive edge in the market by offering exceptional value to retain customer loyalty.

Other emerging trends include:

a preference for subscription-based and direct-to-consumer business models,

the emergence of new consumer-focused technologies,

a focus on convenience in payment options by consumers,

sustainability considerations in purchase decisions,

influence of a shifting demographic balance.

Businesses that can effectively navigate these changes will be well-positioned to lead and thrive in the post-COVID-19 economic environment. In the following sections, we will explore some of these trends in more detail and discuss how businesses can successfully adapt to meet the evolving needs of their customers.

Drivers of consumer behaviour shifts

Technological advancements: “Driving this shift in purchase decisions are consumers’ well-documented digital addictions and growing tech-savvy. Armed with smartphones and internet access, consumers now have reams of information at their fingertips – and the ability to share and explore this information among their trusted online networks and peers. As a result, it has become almost impossible for retailers and manufacturers to ‘manage their messaging and brand equity in the way that they have been accustomed to”- (Deloitte, n.d.).

Ever since the internet's inception in 1983, there has been an unstoppable movement to digitize the consumer journey across various industries. This has led to the emergence of digital-first companies such as Google, Amazon, Jumia, Netflix, Meta, and AliExpress, as well as the expansion of offerings from established tech giants like Apple and Microsoft, and traditional industries such as FMCG and financial services. With internet penetration in Africa currently at 43%, there is a high probability of a further rise in internet access, which will likely accelerate this trend. This presents significant opportunities for businesses to leverage digital technologies to improve customer experiences and build brand loyalty with confidence.

The development of new AI-enhanced tools is helping companies meet the demands of consumers by providing personalized experiences that offer more customised interactions. These AI tools can also be used to influence consumer behaviour, allowing businesses to create more effective marketing strategies with certainty. Moreover, AI tools can prove effective in enhancing consumer decision-making. For instance, ChatGPT, a tool that is being integrated into Microsoft's Bing search engine and Google’s Search Lab, provides consumers with a powerful research tool that can quickly help them find the information they need.

Economic influences: The impact of rising prices on consumer behaviour cannot be underestimated, and it is significant. In 2022, countries around the world faced record inflation rates. This was as a result of several factors, including an increase in money supply from government and central bank interventions during and after the pandemic, supply chain disruptions, and the impact of the Russian-Ukraine war.

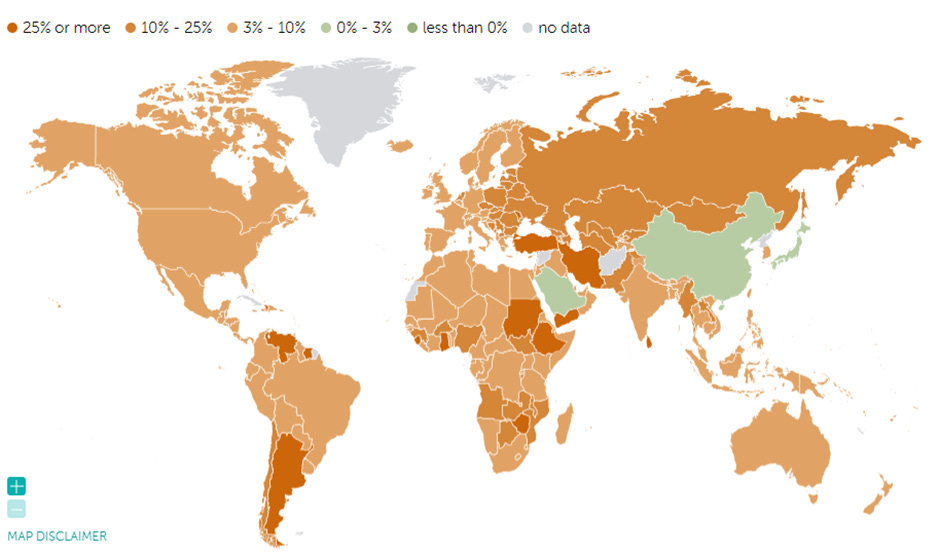

According to the International Monetary Fund (IMF) data, the global inflation rate increased from 4.7% in 2021 to 8.8% in 2022, which is a significant jump. The African continent, which already had high inflation rates, saw an increase from 12.8% to 14.5%, which had a considerable impact on the economies. The map below shows that most countries experienced an average inflation rate greater than 3%.

The impact of rising prices is a global phenomenon that would shape consumer behaviour for the foreseeable future. It is not limited to specific regions or countries, and businesses must be prepared to adapt. As consumers are becoming more price-sensitive, they may seek out cheaper alternatives to mitigate the impact of rising prices on their budgets. This trend is even more profound in Sub-Saharan Africa, where 60% of the world's extreme poverty is concentrated.

Considering this scenario, it is highly likely that consumers will focus more on value-driven purchasing, seeking more affordable alternatives rather than relying on brand name. Therefore, businesses need to re-evaluate their pricing strategies, offer discounts or promotions, and find innovative ways to offer value to customers. Failure to adapt to these changing consumer preferences could lead to a significant decline in sales and market share.

Societal Influence: Though many people claim to be above trends, that, in and of itself, is often a trend. (V and enberg, 2020). Cultural shifts greatly affect the behaviours of consumers. We fall prey to normative social influence when we express opinions or behave in ways that help us to be accepted or that keep us from being isolated or rejected by others. When we engage in conformity due to normative social influence we conform to social norms — socially accepted beliefs about what we do or should do in particular social contexts (Niosi, 2021).

Presently, as the global community is placing greater emphasis on sustainability and social responsibility, consumers' purchasing decisions are increasingly reflecting these values. In developed markets, consumers are seeking out more eco-friendly products, such as electric vehicles and products from sustainable supply chains. A recent survey of adults in the United States showed that nearly two-thirds are willing to pay a premium for products that align with their environmental and ethical values.

How businesses can adapt

Based on the extensive discussion, it is evident that businesses must adeptly navigate and remain updated with the ever-changing consumer behaviour. To accomplish this, they should possess a profound comprehension of the market and emerging trends. Several highly recommended strategies that businesses can implement to achieve this include:

Increase understanding of their customers: The COVID-19 pandemic prompted consumers to adopt new modes of living, shopping, and interacting, but post-pandemic trends have revealed a resurgence of traditional habits in an optimized form. Considering these insights, an omnichannel approach, as opposed to a purely digital strategy, can help businesses better serve their customers and maximize value. In the current economic climate, it is crucial for businesses to consider consumers' inflation concerns as they strive to deliver value. Through continuous market research and customer feedback, businesses can gain a comprehensive understanding of their customer's needs and preferences, which can inform their overarching business strategy.

Staying ahead of the curve with innovation and technology: The results of a 2018 survey conducted by the World Bank indicated that nearly 50% of Nigerian respondents desired to emigrate permanently. Entrepreneurs and businesses can tap into this diaspora population's yearning for a sense of home and nostalgia to create value. Financial institutions could develop innovative products to address the needs of this demographic. By investing in technology and innovation, businesses can stay ahead of the curve, drive consumer behaviour, and offer cutting-edge products and services. Incorporating sophisticated data analytics and machine learning models can provide businesses with valuable insights into consumer behaviour. Making existing systems agile would allow businesses to quickly capitalize on these insights and adapt to an ever-changing world. The application of behavioural science to predict and influence consumer behaviour would be a strategic advantage for businesses.

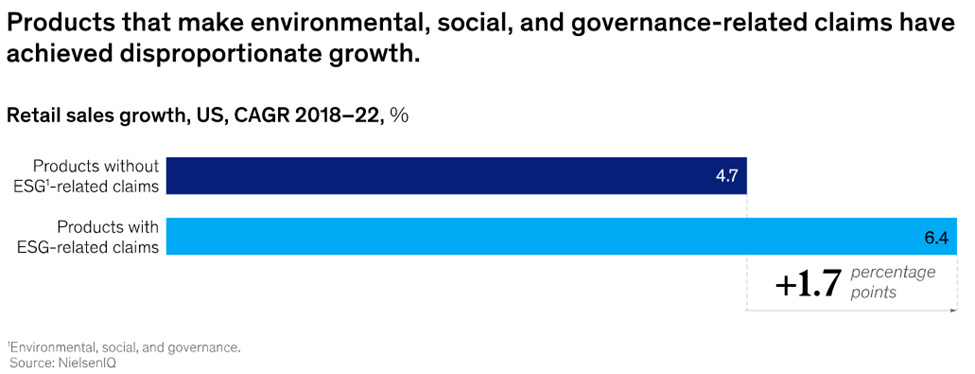

Establishing a strong brand image and reputation: Amidst the evolving consumer demands, having a well-established brand image and reputation can prove instrumental in differentiating a business from its competitors, retaining existing customers, and attracting new ones. A brand that is perceived as innovative, offering personalized customer services, and being environmentally responsible, is more likely to endure and leave a lasting impression. A study by McKinsey showed in a five-year period, products making ESG-related claims accounted for 56% of all retail growth.

I'll end with a quote from the renowned General Electric former Executive, Jack Welch “Change before you have to”.